Hitachi ABB Power

This one is going to be a long one as I am used to writing on much smaller companies but sometimes even larger companies are off the radar so suggest you better grab a cup of coffee or a tea while you read the blog-

Rooibos Tea (Teamonk) - If you love exotic tea flavors this one will you would cherish!

Activated Charcoal Mint Mocha(KC Roasters)- Experiment with your coffee while you can refrain doing that with your stocks for now.

It is raining unicorns in the private space, the force at which the Indian startup disruption is shaping, this year might be the best ever and well deserved too. Moving to the public markets, there are only 335 companies with market cap >1bn USD compared to the already 100+ unicorns in the private space(Link). Trailing financials are increasingly becoming analytical tools rather than valuation deriving raw material and this is certain given the dichotomy of valuation multiples observed in some listed tech platforms vs other traditional companies. Not that all that glitters is gold but we see how the value-growth-tech conundrum is shaping up.

Cutting the chase short, as I tried to write about this company in brief realised it was difficult to summarise it in few paras and from the day I have begun to write on this the market cap may have moved by 30%. But that is not of relevance as it just shows how lazy I have been. Moving to the company, Hitachi ABB Power was demerged from ABB India and listed as a separate company in 2020. Now the global power grid business of ABB is held in majority(80%) by Hitachi Ltd Japan. Almost 40% of ABB (2018) India’s revenue came from power grid business prior to demerger.

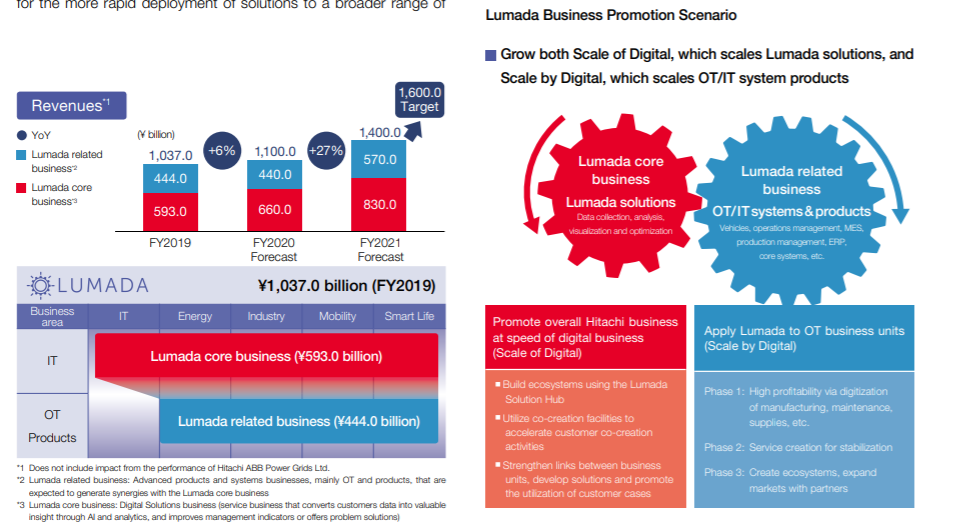

Hitachi contrary to what many think has bulk of it’s revenue coming from IT services-

Why is Hitachi’s revenue composition relevant you would feel, it is very much relevant in how they are thinking of their businesses with the capability to be a tech and digitally enabled company across all verticals. The recent 31 bn USD acquisition of ER&D company Global Logic by Hitachi reiterates the point (Link). They are indeed trying to create a digital platform and more importantly a mindset which would benefit all of its businesses. Lumada which is a digitial soultion platform of Hitachi is another testament of it’s mindset which has turned all of its verticals into IoT enabled tech plays (Link)

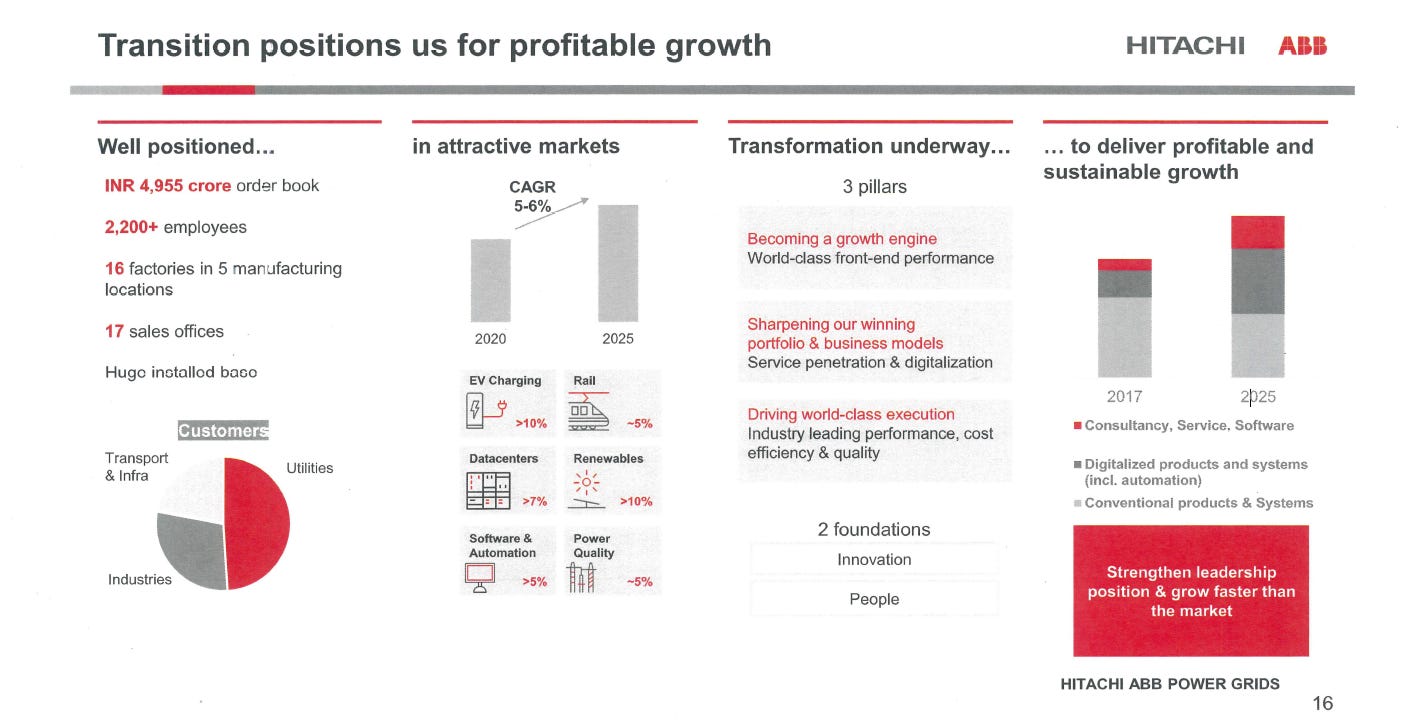

Moving to the Power Grid Business, the global business housed in Hitachi ABB JV is $10 bn +. Hitachi management has aggressive growth projections for the energy biz where the power grid segment is categorised-

As on 2018, ABB’s Power Grids division offered products, systems, software, automation and service across the power value chain, leveraging the local manufacturing footprint and pool of expertise. The company mentioned access to newer geographies and project finance as key reasons to move this division out and I too believe with Hitachi’s expertise this has turned into a tech driven business although it still riles under the insipid order book B2B process. The breakup of product offerings-

Source: Dolat Capital Report

The culmination of IoT, digital mapping of power infra, renewable energy transmission all are tailwinds defining the business potential ahead. Some of the innovations/progress/developments within India and abroad for the company/parent

HDVC Light (ABB is the pioneer in HDVC (Link)

https://www.hitachiabb-powergrids.com/in/en/offering/product-and-system/hvdc

Smart Digital Substation

https://www.hitachi.com/New/cnews/month/2021/02/210224a.html

Solid State Transformer

TXpert Ecosystem for digitalization of transformers

Hybrid Switchgear

Large scale e-mobility solution

Some others discussed in this management interview-

Currently the company has a INR 5k crore order book(Primarily from utilities) to be executed in 15 months. Given the macro tailwinds I expect the order flow to remain good-

On back of the sector tailwinds and change of mix of revenue, I believe the company can double its revenue in the next 5-6 years (not backed by any tedious number crunching). A recent Dolat capital report expects the FY23 Revenue to be 5200Cr+ and the margins may move to double digit too.

Extending the power talk and while we try to learn more on ABB Power, I ran a small screener over the weekend on companies with >2.5k cr sales and Price/Sales>10 (TTM Sales, similar list if take preceding year too), to learn more on the larger companies valued richly and the pattern there. The list had a total of 19 companies and if we exclude financials and real estate 16 companies -

Adani Type (Ports, Green, Transmission, Toys etc) - Midas touch

FMCG companies - Nestle , HUL , Dabur..

Discretionary Consumption - Paints, Food..

Pharma ( Divis, Gland science+persistence)

One relevant comparison was Honeywell auto, it is MNC driven global conglomerate with innovation and forefront of Industrial IoT. It though partners with global software companies for support. (Link). Its 5 year PAT growth is ~30% and margins now late teens.

Is ABB Power the next honeywell? Question for which the answer lies in the future ! But Industrial IOT, cutting edge tech, MNC, global conglomerate sounds too familiar :)

If you enjoyed reading this, go buy me a coffee. Someone challenged me that if 10 people do not buy you a coffee post reading you are not writing well :( !