Hi,

Based on my recent survey relating to which company should I choose for a long form write-up. Over 50% voted for the lesser known listed company Ador Multiproducts Ltd. I have been part of investment research and portfolio management roles over the past 8 years and in my recent role at Roots Ventures have comprehensively analysed early stage brands within the CPG segment covering cosmetics, food and few other sub segments. The fund has invested in 5 emerging brands and a consumer tech platform.

In the 500+ deals evaluated, the problems which most CPG brands faced were relating to uniqueness of SKUs, manufacturing troubles owing to high reliance on contract manufacturers, inability to quickly test and ascertain product market fit and form a strong hold community of users who would love the products. The next obvious hurdle is the distribution which primarily is online for young brands wherein the struggle is to optimize on digital marketing through various portals with limited availability of funds.

Before the deep dive into CPG brands and investing at Roots I have been tracking a little known company from a well known group, Ador Multiproducts. It was a 15cr Mcap then (now it is about 20cr) with stagnated revenues over many years. The thing with nano/micro caps is that everything is never perfect and in most cases it always remains the same for eternity. But few which move, create a rampage in your portfolio but it is easier said than done. A company with revenues around 6-7cr via contract manufacturing and that too with 2 manufacturing setups there was not much to read here. But decided to look a bit deeper and figured the company was trying to do something interesting and without even realising the market potential of the CPG cosmetic ecosystem it was trying to create.

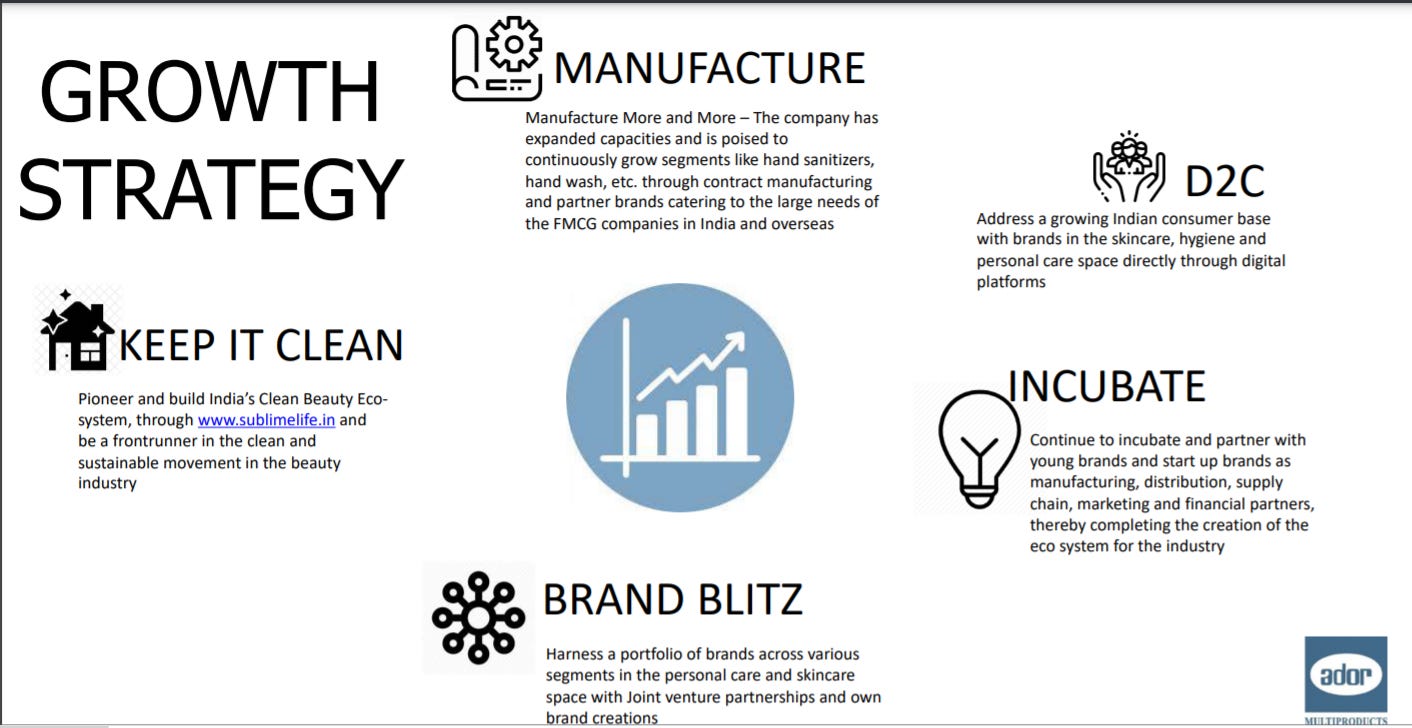

The image from company’s latest presentation gives a good picture on what the company plans to achieve -

Small batch size testing (Helps in getting global brands to India and also with contracts from emerging brands in India)

Contract Manufacturing for Large brands

Developing Own brands

JVs to develop brands in partnership

D2C clean cosmetic platform

Until the pandemic company’s contract manufacturing capacity was highly under utilised , but given the surge in use of sanitisers the company could clock close to 7 crores of revenue in a quarter as against a year. The company has alcohol, pharma and Ayush licenses within the cosmetic domain. Even if we consider the surge is temporary the market size of sanitisers has grown exponentially owing to the pandemic. And the revenue has been just from a single manufacturing facility as the company has sold off the Bangalore plant and can use the same for other segments.

The company has started batch size testing and manufacturing which I believe will pave way for growing its small contract manufacturing business at a good speed as it enables to offer this service to lot of small brands in India as well as global brands. India has been an under branded country but given my experience in evaluating brands things are changing at a frantic pace in the D2C space as younger brands are disrupting existing markets (Just Herbs) or creating a new market altogether (Beardo). Ador has a tie up with Amazon to develop a Man’s grooming brand and also recently launched a JV with Ravi Shastri to launch 23 yards. (Just to give perspective Beardo was sold at a 5x sales multiple at ~400cr to Marico). Ador has also tied up with UK brand Anatomicals wherein it was a distributor initially to being a brand JV partner now. It also has a small stake in a kids cosmetic brand Cocomo which is a growing segment.

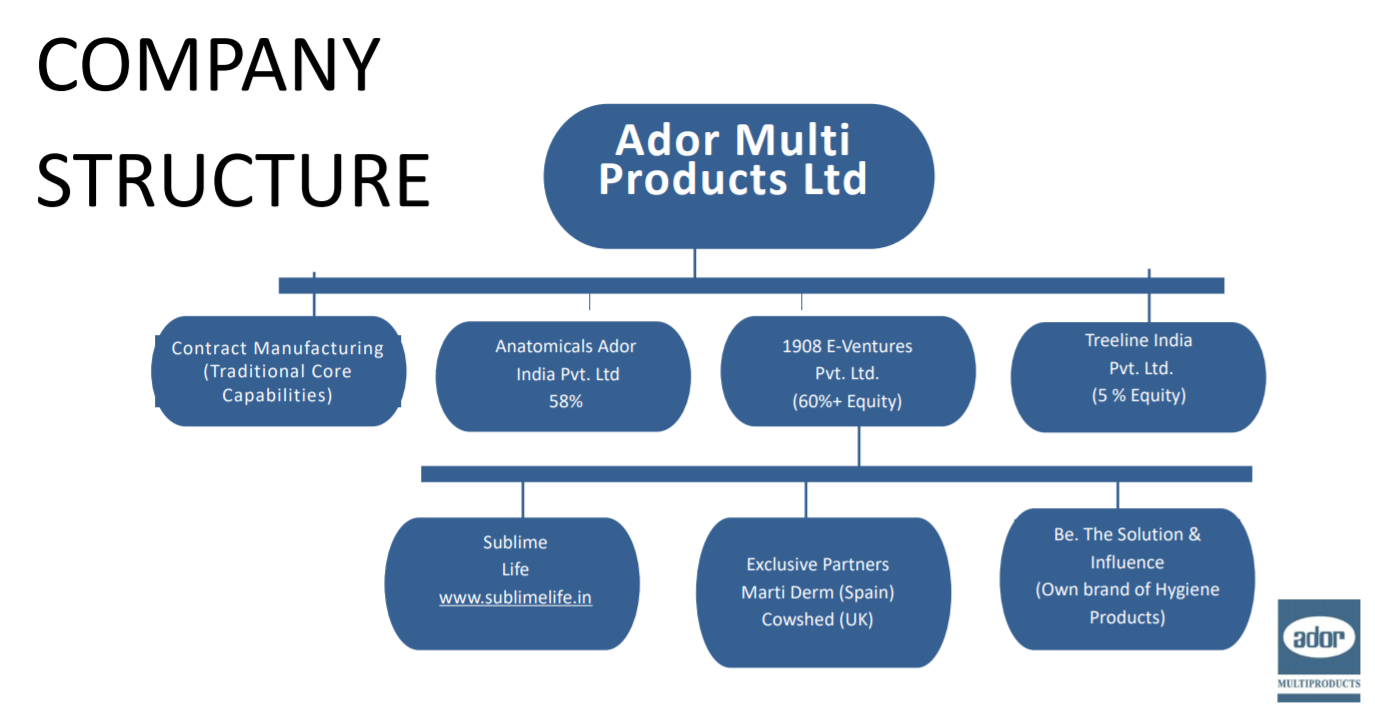

This chart gives a good visual on the company’s structure -

Coming to the last and personally the most interesting part of the company, Sublime Life(SL) which is an online platform which houses many clean cosmetic brands (Indian and foreign). The portal houses 50+ brands currently across different sup categories. It has 12k Instagram followers and slowly building a community of like minded believers in clean cosmetics.

The growth of clean cosmetics is rapid on a small base and a niche target audience but SL is one of the largest market place for the same. Even larger brands like Colorbar, Lakme, Estee Lauder etc are paying heed to the segment with new launches around the clean beauty theme. SL could be a house for emerging and established brands with clean cosmetic range. The company is also leveraging this platform to build up a community which is inspired by this concept and enables Ador to also sell its own as well as JV brands on the platform indirectly giving a D2C push to all its brands. If I were to evaluate SL as an isolated investment given the growth in this segment, the market cap would be a small price to pay just for it.

With the entire surrounding ecosystem built, this is nothing short of a micro CPG fund with manufacturing and distribution capabilities. Although there are lot of uncertainties around execution which the company is able to achieve in the past 2 years. In the best case scenario the company could have a revenue of 100 crores in the next 5 years with a strong digital distribution platform and could be valued at 5x sales. In the worst case company might just have a revenue of 30-40 crores and valued at 2x sales . In either case the risk return payoff is huge considering the current market cap. Although reiterating that with Microcaps/nanocaps risk of patience alongwith the usual money risk is more often than not very High.

Disclosure: This is not a buy recommendation but just educational content to evaluate a company. It is safe to assume that the author holds shares in the company discussed and views could be biased. The company is part of GSM-2 category of the exchange currently and has addtional margin requirements.